At 22, I Bought Medical Insurance for RM113.33. A Similar Plan Now Costs RM59.80 [SPONSORED]

In the early 2010s, 22-year old Suraya got herself medical insurance as her first protection product. She started paying RM113.33 per month for a medical insurance that comes with RM190,000 annual limit*.

(*Annual limit is the maximum amount the insurance will pay in one calendar year. For example, if my medical bill comes up to RM190,010, then I will have to pay RM10 out of pocket – the rest are covered)

Fast forward to 2022, a 22-year old non-smoking woman only has to pay RM59.80 per month for medical insurance with RM150,000 annual limit under the Tune Protect PRO-Health Medical plan.

RM59.80! That’s near half of what I paid! I could have saved more money if this plan was available back then. I could have had more fun.

Why did I Get Medical Insurance as My First Insurance?

To be honest, I wanted comprehensive insurance from the get-go. I knew getting protection was one of the most responsible things to do when I became an ‘adult’ (aka graduated from school, entered the workforce, yada yada).

Back then, there was no such thing as buying insurance online, and no way to know the price unless you contacted an agent. So I contacted one and asked him to quote me the most comprehensive, all-in plan possible.

The quotation came: over RM500 a month.

My heart dropped. I could NOT afford it, not on my small salary then. So my agent asked me to re-prioritise – what am I most worried about?

I said, my biggest worry is suddenly being admitted to the hospital, presented with a huge medical bill and depleting my parents’ retirement savings. I don’t want to be a burden to them, they have already sacrificed so much for me.

Ah, then perhaps you can start with stand-alone medical insurance, he said.

That’s why I got medical insurance as my first insurance. Of course, the other types of protection – life, critical illness, personal accident and the rest – are all important too, but I had to prioritise.

Strategy: If You’re On A Budget, Get Some Coverage First & Upgrade as You Go Along

I believe the hard part about buying insurance is this: wanting the best plan and coverage, but budget constraints (who doesn’t have this?) forces you to pick a good enough plan for now, and upgrade as you go along.

That’s what I did. I got medical insurance first and started paying RM113.33 per month for it. Over the years, as my income grew, I slowly added other types of protection as I could afford them, and upgraded my existing plans.

(It is recommended to review your protection plans every few years anyway)

Don’t let other people scare you into thinking you MUST get the best medical insurance possible with the highest annual limit (RM1mil and more) OR NOTHING. This isn’t helpful. Good enough coverage that suits your budget is better than no coverage.

Sure, there’s a chance something *might* happen to you and you get hospitalised and the bill comes up to six-figures. But these instances are rare. Outliers. 0.001% of cases.

According to the Tune Protect team, the average and median claim for medical insurance is only RM12,000. Chances are, *if* anything happens, RM30k-150k coverage is enough to cover it.

Again: if you’re on a budget, get some coverage first. You can always upgrade later (though not always – but again, these are statistically rare cases).

What does medical insurance cover anyway? What am I getting? What am I NOT getting?

I have spent countless hours learning about medical and health insurance/takaful from individual agents, my year-long CFP course, the Life Insurance Association of Malaysia website and directly from the folks at Tune Protect themselves.

There are a lot of things to know before getting medical insurance, but these are your MUST-KNOW information, divided into three parts:

- Part 1: What medical insurance covers

- Part 2: What medical insurance DOESN’T cover

- Part 3: Why medical and health insurance/takaful prices WILL increase

Let’s go!

#1 – What Medical Insurance covers

Medical insurance pays for your hospitalisation and surgical bills. That means, if something happens and you require admission to the hospital, you may worry about your health but at least you don’t have to worry about paying the bill (subject to what’s covered in policy).

Different insurance/takaful providers may offer variations in their medical insurance products, however arguably the most important details are:

- Annual limit – You will see a wide range, from RM30k to RM1.5mil and above. Higher is technically better, but some coverage is better than no coverage

- Lifetime limit – unlimited is best

- Inpatient vs outpatient – Simplistically, inpatient means you must stay in hospital (serious case) while outpatient means you can be treated at home (not as serious). The former is more expensive and should be prioritised over the latter.

- Uncovered conditions – some conditions that are usually not covered include pre-existing conditions, pregnancy-related conditions, accidents due to high-risk activities, plastic surgeries, mental illness and more

- Standalone or rider – You can get medical insurance on its own or as an add-on to your life insurance/takaful plan

There are more details of course, but I’m just listing what I think are the most important ones. All the variables will affect the price, so do look for the best possible combination for your budget rather than the lowest possible price.

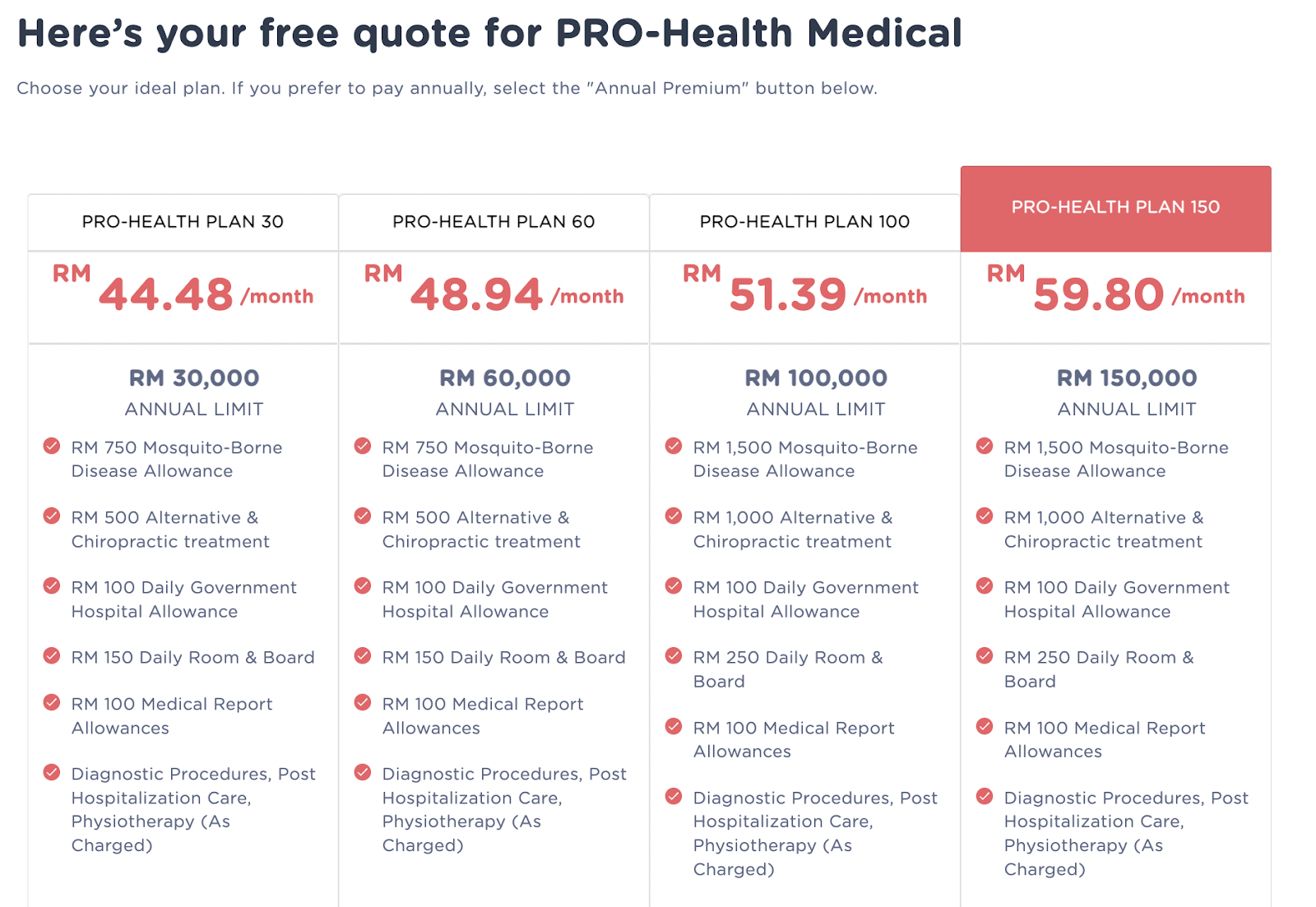

I’ll give you an example. Here is my quotation from Tune Protect PRO-Health Medical, based on personal details:

- 35 years in next birthday

- Female

- Non-smoker

You can see that:

- Annual limit: RM30,000-RM150,000

- Lifetime limit: unlimited (found this info in the policy document)

- Inpatient vs outpatient: Inpatient (unless stated on product page, assume inpatient)

- Standalone or rider: Standalone (rider means you HAVE to take life policy also)

- Daily room and board: RM150-RM250 per day

- My quotation for RM30,000 annual limit plan: RM46.19 monthly / RM527.85 yearly

- My quotation for RM150,000 annual limit plan: RM65.45 monthly / RM748.00 yearly

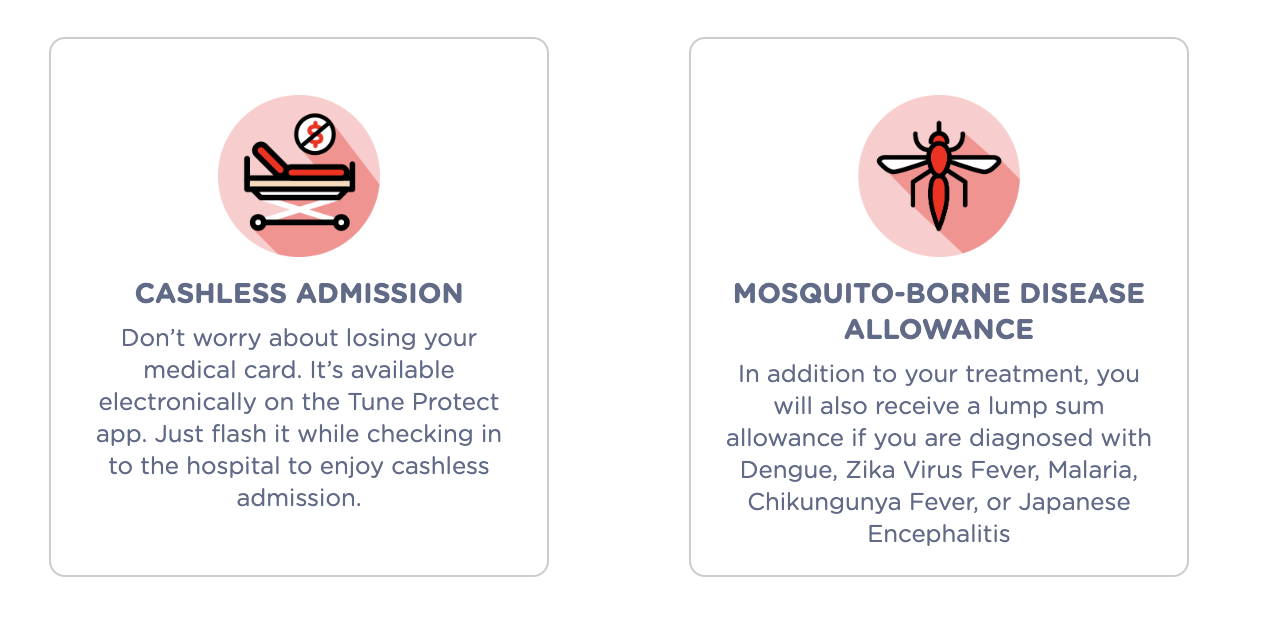

- Extras: Cashless admission; Mosquito-borne disease allowance; Alternative & Chiropractic treatment; Daily government hospital allowance; Medical report allowance

Note: My quotation =/= your quotation. As a general rule, your quotation will differ based on your gender, age and smoking status. Older and smoking males will be quoted the highest premium.

#2 – What Medical Insurance DOESN’T cover

“I took medical insurance but they didn’t cover for…”

It’s annoying, isn’t it, when the product doesn’t work as you thought it would?

However, in this case, chances are your claim was denied because what you are claiming for is instead covered under another type of medical and health insurance/takaful, and not under medical insurance. After all, medical insurance is just one of four types of medical and health insurance/takaful.

Let’s do a simple ‘is this a medical insurance’ table.

Is this medical insurance?

| Medical and health insurance/takaful | Is this medical insurance? |

| 1) Hospitalisation and surgical insurance/takaful provides reimbursement of actual medical expenses incurred in the event of hospital treatment / surgery for covered conditions. This amount is subject to the annual or lifetime limit fixed by the product plan. | Yes, this is medical insurance |

| 2) Dread disease, or critical illness insurance/takaful provides a specified lump sum benefit upon the diagnosis of any of the 36 listed conditions specified in the policy such as cancer, heart attack, stroke, kidney failure etc, or actual undergoing of a surgical procedure such as coronary artery bypass surgery, heart valve surgery, brain surgery etc. | This is critical illness insurance/takaful, NOT medical insurance. |

| 3) Disability income insurance/takaful covers a portion of your income in the event that you are displaced from work when stricken with an illness or an injury. | This is income replacement, NOT medical insurance |

| 4) Hospital income insurance/takaful pays a specified sum of money per day of hospitalisation for any covered illness, sickness or injury. This amount is subject to a maximum number of days per disability. | This is daily income benefit, NOT medical insurance |

Source: Part 1 of MHIT education article series by LIAM

As you can see, a medical insurance ONLY pays your hospitalisation and surgical bills, and DIRECTLY to the medical service provider. You DO NOT get any other lump sum or cash money, unless specified OR if you purchased other types of medical and health insurance/takaful as well.

#3 – Medical and health insurance/takaful prices WILL increase

Unfortunately, it is highly likely that the price of your medical insurance and other medical and health insurance/takaful will increase every few years.

This will happen to everyone. To me as well. Remember I said I got my medical insurance with RM190,000 annual limit for RM113.33 per month? Well, I’m paying RM170 for it now. Exactly the same plan, just higher price.

The reason for that is due to this annoying thing called medical inflation.

Medical inflation in Malaysia is high. VERY high.

You must know that insurance and takaful companies don’t want the increase to happen. Customers hate it.

However, takaful/insurance providers have no choice but to do it, because according to Bank Negara Malaysia’s Managing Medical Claims Inflation document, the medical inflation rate in Malaysia in 2019 alone was 13.2%.

13.2%!!

Yes, 13.2%! That is a VERY high number. If it goes on, and it likely will, that means the average medical claim will double in around five and a half years (using the rule of 72).

To put that into context, the same procedure that costs RM50,000 in early 2023 will cost:

- RM100,000 by mid 2028

- RM200,000 by early 2034

- RM400,000 by end of 2039

So do you see why insurance/takaful companies had to reprice 4.5 million certificates/policies between 2016-2019? They can’t afford not to.

In conclusion: Just get whatever you can afford right now

Fact: Many Malaysians are underpaid. Chances are you can’t afford to spend hundreds on insurance right now. Many Malaysians also lack time and expertise to research insurance and compare quotations and all that.

Remember – whatever you can get on your budget, which you can realistically afford to pay every month is good enough. If you can only afford RM50 or so right now, go for the RM50 per month plans.

I didn’t have the RM50 per month plan when I was 22, but you do. You can get affordable insurance and microinsurance directly from insurance/takaful companies. Getting a quotation is so much easier – just key in some basic details at Tune Protect PRO-Health Medical.

As someone who took weeks to find my own medical insurance last time, let me just confirm the convenience of online products. Purchasing takes just a few minutes. No hassle, no long forms to fill, no endless questions or 3rd party. You can even get a 15% immediate discount too!

TuneProtect in particular takes customer journey and convenience seriously and implements the 3-3-3 Brand Promise:

- 3 minutes to buy

- 3 hours to reply

- 3 days to receive claim upon approval

To make your life even more convenient, download the Tune Protect app (available in Google Play & App Store) to easily manage your policies, make claims, access your e-medical card and locate panel hospitals quickly. PRO-Health Medical is eligible for income tax relief.

‘Med’ About Health Campaign [ENDS DECEMBER 2022]

If you purchase Tune Protect PRO-Health Medical before the end of December 2022, you are guaranteed to get a RM80 Decathlon e-voucher for FREE.

If you are extra lucky, you may also win an Apple Watch worth RM1,899. Learn more about this campaign here.

Hope this article helps you. If you have experience with medical insurance, and have additional tips to share, please leave a comment below 🙂 If you’re travelling soon, make sure to get travel insurance.

![What You Need to Know About Payment Relief Assistance [SPONSORED]](https://i0.wp.com/ringgitohringgit.com/wp-content/uploads/2021/07/payment-relief-assistance-alliance-bank.jpg?fit=768%2C384&ssl=1)