My Total Income and Expenses in 2020

Welcome back to my total incomes and expenses report, now in its fifth year! In this annual series, you will see a review of my financial year- how much I earned and what I spent on throughout the year.

The financial data presented here is nowhere near perfect (but perfect is boring and not to mention impossible), but I love that I can share this information with you, so you get to see how record-keeping is beneficial in practice.

This article is divided into two big sections: incomes (recorded via a Google spreadsheet) and expenses (recorded via my expense-tracking app). If you’re a regular reader, you should already be familiar with my expense breakdowns anyway – I post them every month.

Income in 2020

I earn my living from various income sources, which you can check here: [VIDEO] My 8 Sources of Income As a Malaysian Blogger

In 2020, I recorded RM71,149.42 in gross income (not nett profit). Remember, I’m self-employed, so I have business-related expenses.

If you take out business-related expenses in 2020 (RM31,874.32; breakdown in Expenses in 2020 section below), I effectively earned RM39,275.10 or RM3,272.93 per month in 2020.

The amount is lower than I wanted, but hey. The fact that I still had work in the first year of pandemic is already something to be grateful for.

I know I should have done something to earn more and hit my RM100k nett profit goal so I can brag about it but to be honest my mood to earn kind of dissipated during the pandemic and never came back :/ I wonder if any of you feel the same. I know I’m not particularly ambitious in the first place but this lack of semangat is somewhat worrying.

Expenses in 2020

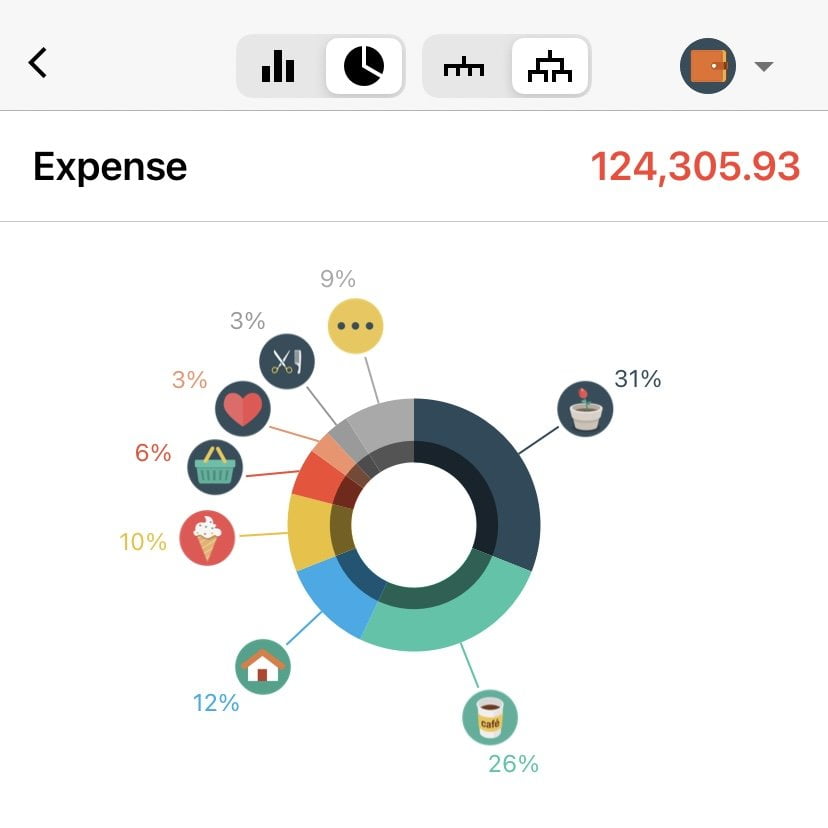

According to my expense tracker, I spent RM124,305.93 for the whole of 2020. If you exclude business-related expenses (RM31,874.32), I effectively spent RM92,431.61 or RM7,702.63 per month in 2020.

Yes, I spent more than I made in 2020. More than twice over. I broke the #1 personal finance rule, earn > spend, and I’m not even sorry about it.

For one, I’m happy with what I spent on. I remained frugal except for one category, which I spent lavishly on – Donations & Gifts. I’ll expand further below.

Secondly, 2020 was an absurdly good year for my investments – my net worth still grew despite me overspending. It’s absurd and ridiculous and yes I’m lucky AF that things turned out well. I’ve decided not to keep all that luck for myself and didn’t want to hoard money for hoarding’s sake, so I spent it.

Here are my expenses in 2020 sorted by categories, from highest to lowest:

Breakdown and comments on each expense category

1) Donations and Gifts – RM37,547.23 or RM3,128.94 per month, on average

Before you say, oh wow Suraya that’s a lot – let me just stop you – I’m not *that* altruistic. Sure, I paid my zakat and made small donations to various charities, but the majority of my Donations and Gifts went to my family. In 2020, I:

- Paid my parents’ electricity bill (it’s around RM800-900 per month.. I know.. I’d love to lower this expense but I also know they use a lot of aircon so I can’t say anything, I want them to be comfortable..)

- Paid for renovations for a room at family home (also used as bridal room, so really I benefited a lot from this)

- Contributed to my dad’s dusun project at kampung land

- Gifted an expensive massage chair to mom for her birthday (shared with sisters)

- Contributed to meals and gifts for celebrations like birthdays etc

Even though I regret none of these expenses – after all, much of the money ultimately flowed back into the economy, which is good yes? – I do want to balance this giving spirit with a dash of reality. I was lucky that 2020 has been a financially good year for my investments therefore my finances are still strong, but I know I can’t keep this up if I continue to earn the same income.

2) Business – RM31,874.32 or RM2,656.19 per month, on average

Because you need money to make money. Things I paid as business expenses in 2020:

- Facebook ads

- Ezoic Premium, an ad-optimisation software

- Book re-printing for Money Stories from Malaysians Volume 2

- Hosting and domain renewal

- Various marketing tools

- Memberships to organisations

- Books

- New website design

- And a new business venture which I don’t want to expand on yet 🙂 Watch this space

3) Utilities & Rent – RM14,517.61 or RM1,209.80 per month, on average

Bless my landlady, during when MCO 1.0 hit, she agreed to waive 1 month rental for me.

4) Wedding – RM12,062.09 or RM1,005.17 per month, on average

Temporary category, obviously 🙂 Again, thanks for all the well-wishes!

Related: I Spent RM12,062.09 For My MCO Wedding (Cost Breakdown Included)

5) Groceries – RM7,166.25 or RM597.19 per month, on average

Spending almost RM600 per month on groceries is more than worth it, considering the joy, source of creative outlet and health benefits I get out of the whole process.

I wonder how much my groceries will now cost, now that I’m buying for 2 people. Common sense says it’ll double, but let’s see.

6) Dates/Travel – RM4,910 or RM409.17 per month, on average

I barely went anywhere in 2020 (though admittedly nor do anyone else). Much of this expense were recorded in December, when we went for a honeymoon in Langkawi.

(Defensively, I have to say this: we self-quarantined for 2 weeks after returning home)

7) Misc Wants – RM4,217.25 or RM351.44 per month, on average

Misc Needs is a category for those random ‘nice to have’ purchases. Not strictly necessary, but I still wanted them. I didn’t realise it, but I bought quite a lot in 2020. Small expenses really do add up.

In 2020, the following expenses got logged as Misc Wants:

- Netflix

- Books

- Clothes

- Makeup and skincare

- Hair perm

- Massages

- Home decor

- Courses

- Jewellery

- Teeth whitening session

- Steam games

- House plants

Alright, I have to be mindful of this expense. I can’t keep using pandemic-induced anxiety as an excuse to keep buying unnecessary stuff.

8) Misc Needs – RM3,128.96 or RM260.75 per month, on average

Misc Needs is a category for random ‘must pay’ things that don’t really fit elsewhere. I have to pay these, or I’ll either go to jail or my professional life will be jeopardised.

In 2020, the following expenses got logged as Misc Needs:

- Tax payment

- Renew driving license

- Home maintenance and organisation

- Replacing home appliances (my kettle died TWICE ahahaha)

- Office chair

- Masks and sanitiser gels

- Stocking up on toiletries and skincare

- Fire extinguisher

- Financial calculator for CFP

- Credit card service tax

- And other misc stuff

9) Insurance and Medical – RM2,339.89 or RM194.99 per month, on average

Added on Critical Illness plan since November 2020. Currently, my monthly commitment for insurance is:

- Medical card – RM113.33

- Personal Accident – RM53

- Critical Illness – RM172

Related: 9 Things You MUST Know Before You Buy Insurance in Malaysia

10) Public Transport – RM1,827.42 or RM152.29 per month, on average

… Not a bad amount, for someone who doesn’t have a car. Mostly spent on Grab rides and renting cars.

Related: SOCAR Review: 7 Tips to Get Cheap Car Rental in KL, Penang and Johor

11) Social – RM1,477.50 or RM123.13 per month, on average

Treated family and friends to meals.

12) Food – RM1,237.20 or RM103.10 per month, on average

I track Food expenses as (1) they correlate to weight gains and (2) are NOT part of groceries, dates, travel or social activities.

RM103.10 per month is quite high for my taste. Something to lower in 2021.

13) Pets – RM1050 or RM87.52 per month, on average

Worthwhile expense. The buggers make me happy.

14) Mobile – RM950 or RM79.17 per month, on average

My data consumption pattern fluctuates, but I know I need around 70-100GB per month.

One of the things planned in 2021 is moving to our new home, where we’ll invest in home wifi, which means this expense will be significantly lower around Q4 or 2021 or so.

I like that Yoodo gives me the flexibility to increase/decrease my data as my data needs change. If you want to try Yoodo out too, get free data when you sign up using my referral link.

Conclusion and self-reflection

Annual savings rate (aka percentage of income saved; higher is better):

- 2017: 39.77%

- 2018: -48.95%

- 2019: 14.1%

- 2020: -135.34%

If I’m an investment, you should stay far away from this kind of performance. Volatile AF. No consistency.

But that’s life. We can learn all the personal finance theory available and still make ‘bad’ financial decisions. In my case, I know that I should have earned more than I spent but I didn’t, and in fact I increased my spending. The only reason why my finances are still OK is because of savings plus amazing ROI from investments.

What will 2021 bring? Will I continue to be lucky? Or will the luck run out? Either way, I know the only way to be financially safe in any financial climate is to have sellable skills. No matter how lazy apathetic about work I may be, I have no choice but to find new areas to love and be passionate about (some which I included in my 21 for 2021 list).

Well, that’s the end of it. Thank you for reading my income and expense report, folks. How was your 2020 like, financially speaking? What tweaks are you making to incomes and expenses, going forward? Let me know in the comments section!

Related:

- My Total Income and Expenses in 2016

- My Total Income and Expenses in 2017

- My Total Income and Expenses in 2018

- My Total Income and Expenses in 2019

Suraya is definitely the most transparent ever blogger in Malaysia. 😛

Love this kind of transparency. And let’s work harder in 2021!

Aspire to do something similar to this kind of income report in near future.

Eagerly await that post from you!

Hi Suraya, may I know which web hosting you use?

I want to start a blog and I’m quite confused on which to choose (there are soooo many out there)…

Any additional advise you have for me?

Hi Hui Ting,

It’s a bit outdated, but please check out my step-by-step guide on earning money from blogging – https://ringgitohringgit.com/blogging/earn-money-from-blogging/. You don’t have to start with paid hosting. Start with free and go from there.

Unless of course if you already have an audience and ready to start with paid hosting. In that case, I use Siteground. Exabytes is another good option: https://www.exabytes.my/web-hosting/wordpress-hosting